The Baby Boom Generation will never be mistaken for the Greatest Generation that survived the Great Depression and defeated evil in a World War that killed 72 million people. I hate to tell you Boomers, but putting a yellow ribbon on the back of your $50,000 SUV is not sacrifice.

Our claim to fame is living way beyond our means for the last three decades, to the point where we have virtually bankrupted our capitalist system. Baby Boomers have been occupying the White House for the last sixteen years. The majority of Congress is Baby Boomers. The CEOs and top executives of Wall Street firms are Baby Boomers. The media is dominated by Baby Boom executives and on-air stars. We have no one to blame but ourselves for the current predicament. Blaming Franklin Roosevelt or Lyndon Johnson for our dire situation is a cop out. Baby Boomers had the time, power, and ability to change our course. We have chosen to leave the heavy lifting to future generations in order to live the good life today.

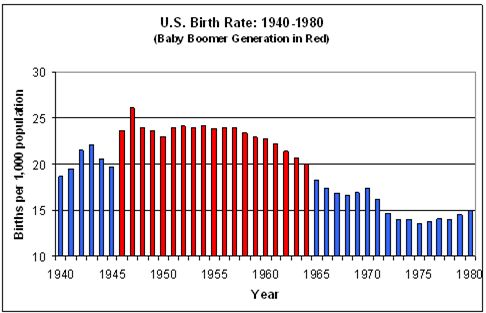

Of course, not all Baby Boomers are shallow, greedy, and corrupt. Mostly Boomers with power and wealth fall into this category. There were 76 million Baby Boomers born between 1946 and 1963. They now make up 28% of the U.S. population. Their impact on America is undeniable. The defining events of their generation have been the Kennedy assassination, Vietnam, Kent State, Woodstock, the 1st man on the moon, and now the collapse of our Ponzi scheme financial system. They rebelled against their parents, protested the Vietnam War, and settled down in 2,300 square foot cookie cutter McMansions with perfectly manicured lawns, in mall infested suburbia. They have raised overscheduled spoiled children, moved up the corporate ladder by pushing paper rather than making things, lived above their means in order to keep up with their neighbors, bought whatever they wanted using debt, and never worried about the future. Over optimism, unrealistic assumptions, selfishness and conspicuous consumption have been their defining characteristics.

click to enlarge images

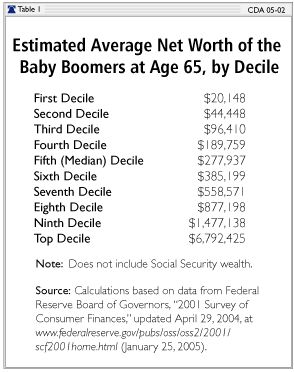

Boomers are currently in their prime earning and spending years. A Baby Boomer turns 50 years old every 7 seconds. The older Boomers had a fantastic run from 1989 through 2004. Median net worth for those between the ages of 55 and 59 rose 97% over 15 years to $249,700 in 2004. Median income rose 52%. The younger generation between the ages of 35 and 39 saw their median net worth fall 28% to $48,940. Their median income dropped 10% over the same 15 year period. It is clear that all Baby Boomers are not created equal. Based on calculations made by the Federal Reserve, at least 50% of Boomers will not have a happy retirement. The bottom 30% will reach the age of 65 with net worth of less than $100,000. They will try to subsist in poverty, dependent upon social security and part time Wal-Mart jobs until they die penniless. The top 30% will retire to lives of luxury and leisure. The middle 40% will muddle through with social security payments the only thing keeping them from an old age in poverty.

We have become a have and have not society. Our economy favors education, entrepreneurship, and creativity. Those benefitting from a good education will make dramatically more money than the uneducated laborers. The top 20% of households make 12.5 times the lowest 20% of households. This ratio was 7 to 1 in 1982. The top 1% of households make 20% of all the income in the U.S., the highest rate since 1928. Does this statistic portend a decade long depression? The difference between now and 1928 is the huge household debt burden of Americans. This usage of debt by the poor has masked the gap between haves and have nots for the last 20 years.

As I drive to work every day in my fully paid for 2002 CRV with 110,000 miles, I have plenty of time to observe my surroundings. Sitting in traffic on the Schuylkill Expressway, I have noticed that the number of luxury Mercedes, BMW, Cadillac and Lexus vehicles seems out of proportion to the number of wealthy people in the Philadelphia population.

When I see an older gentleman, wearing a suit, driving one of these automobiles, I assume that he is a wealthy executive who has put in his time and rewarded himself with a luxury vehicle. But, most of these vehicles are being driven by Joe the Plumber types. As I take a shortcut through some of the more depressed areas of West Philadelphia, I see people talking on their Apple (AAPL) iPhones, Direct TV satellite dishes attached to dilapidated row homes, and Cadillac Escalades & Mercedes parked on the mean streets. This is not exactly the world that Henry Fonda’s character, Tom Joad, described in The Grapes of Wrath:

I'll be all around in the dark - I'll be everywhere. Wherever you can look - wherever there's a fight, so hungry people can eat, I'll be there. Wherever there's a cop beatin' up a guy, I'll be there. I'll be in the way guys yell when they're mad. I'll be in the way kids laugh when they're hungry and they know supper's ready, and when the people are eatin' the stuff they raise and livin' in the houses they build - I'll be there, too.

When I see “poor” people appearing to live a more luxurious life than myself, I don’t feel jealous. The thought that goes through my head is: Which banks or finance companies were foolish enough to loan these people the money to live this lifestyle? These foolish financial institutions will never get their loans repaid. What does bother me is that the Bush-Paulson-Pelosi Bailout of Stupid Banks will use my taxes to buy these bad loans from the foolish banks.

So, who is the fool in this scenario? The “poor” person got to drive a Cadillac Escalade for a period of time, the foolish banks got bailed out, the bank CEOs took home $30 million, and I lived within my means and footed the bill for the reckless actions of others. It appears that the fools are the Americans who lived their lives according to the rules. The anger is building. I don’t think the politicians running this country realize what true anger looks like. They are used to Americans being herded along like passive sheep.

I’ve heard many Republican ideologues blame the current crisis on the people who took the subprime loans for home purchases. I’ve also heard many Democratic ideologues blame the crisis on the regulators. The ideologues are wrong, as usual. If a poor person has no home, no vehicle, and no prospects; then a bank tells them that they can buy a $300,000 home, drive a $55,000 Mercedes SUV, and live like people on TV; why wouldn’t they say yes? What is their downside? If you have nothing and “The Man” offers you the American Dream, you’d actually be foolish to say no. Now that they have lost the home in foreclosure and the repo man has taken the Mercedes, they are exactly where they were a few years ago with no home, no vehicle and no prospects.

The regulators were certainly asleep at the wheel. They did not enforce existing rules, foolishly waived leverage rules for the biggest investment banks, and believed that the banks would regulate themselves. They were wrong, but they never made a single loan. The commercial banks, investment banks, auto finance companies, and credit card companies made the ridiculous loans to people who could never pay them back in the search for short term profits. Greedy Wall Street executives created an artificial market for the loans in order to generate billions in fees so they could enrich themselves through stock options and obscene bonuses. They spent their false riches on $2 million NYC penthouses, $100,000 Porsche 911s, and $5 million beachfront estates in the Hamptons. Based on the estimated $2 trillion of losses that our banks have generated, the CEOs certainly deserved annual pay 500 times as high as the average worker. There is no way an “average” worker could possibly be talented enough to lose $2 trillion. You would need to be truly extraordinary to lose that much.

CEOs’ average pay, production workers’ average pay, the S&P 500 Index, corporate profits, and the Federal minimum wage, 1990-2005 (adjusted for inflation):

(Note: You can view every article as one long page if you sign up as an Advocate Member, or higher).