According to the ICSC, about 150,000 stores are anticipated to shut down in 2009, which adds to the 150,000 that closed in 2008 and 135,000 in 2007. Normally, 110,000 to 125,000 new stores open per year. At least 700,000 retail jobs will be lost. The opening of new stores will grind to a halt in 2009. Some major retailers that have closed or will close include: Circuit City -728 stores; Linens N Things - 500 stores; Bombay Company- 384 stores; Sharper Image-184 stores; Foot Locker (FL) -140; Pacific Sunwear - 153. Other large retailers are closing underperforming stores and scaling back expansions plans. By 2011, at least 15% of the existing retail base will have gone to retail heaven. With the amount of vacant stores likely to reach in excess of 200,000 and vacancy rates of new malls already at 28%, there will be no need for the construction of new stores for many years.

Most of the retailers that are closing, lease their locations from mall developers like General Growth Properties (GGP), Simon Properties (SPG), Mills Corp. (MLS), Pennsylvania REIT (PEI), Vornado Realty Trust (VNO). These developers have a quadruple whammy hitting them in 2009. Many borrowed heavily to finance massive mall expansion. The term of these loans were generally five to seven years. The Wall Street whiz kids and their CDO machine generated the vast preponderance of financing in the last five years. According to commercial real estate expert Andy Miller, the collapse will come more rapidly than the residential collapse.

By contrast, in the commercial world, the properties are fewer and much bigger. For example, you may have ten properties in a commercial pool that ultimately works its way into CDOs. Those loans are huge. You may have a shopping center loan in there for $25 million and an office building loan for $30 million dollars. As a result, if you have a default on just one of those loans, you can effectually wipe out all of the subordinate tranches. And that is why when you see the problems begin to appear on the commercial front, it's going to be a much quicker sort of devolution than we saw on the residential side. In the commercial world, most of the financing that happened outside of the apartment business was done by conduits, and there are no more conduits left, and conduits were doing the stupidest loans you could find. They were doing an advertised 80% loan-to-value, which was usually more closely aligned to a 100% loan-to-value. They were dealing with no coverage. They were all non-recourse loans. Many of them were interest-only loans. Those loans are now gone. You can't refinance them, and if you could, the terms would be onerous.

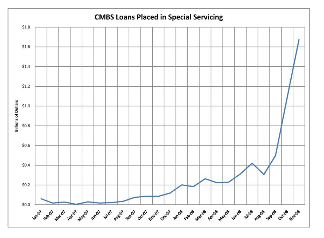

Billions of dollars in debt need to be refinanced in the next two years and there is no one willing to make those loans. The major mall developers are so terrified they have made an all out press to get their fair share of the TARP. As retailers go bankrupt, vacancy rates have reached 9.4% for shopping centers, according to CoStar Group. With virtually no demand, rental income is plunging. With cap rates eroding and operating expenses going up, a perfect storm will hit mall developers in 2009.

The negative feedback loop will accelerate as the year progresses and will spiral out of control by late 2009 and early 2010. The negative feedback loop will lead to major developer bankruptcies and ultimately to Ghost Malls, particularly in the outer suburbs. The positive feedback loop that got us here, made people feel wealthy, smart, and overconfident. It was awesome! The negative feedback loop is going to suck. The collapse of developers will result in more major write-offs by regional banks that financed their expansion. This go around, many smaller regional banks will feel the major pain. The U.S. taxpayer will be required to step up to the plate again and assume financial responsibility for their own lack of spending. Talk about screwed if you do, screwed if you don’t.

Mall owners and commercial developers are on the brink of bankruptcy. Commercial developer CB Richard Ellis (CBG) didn’t sound too optimistic in a recent 10Q filing:

We are highly leveraged and have significant debt service obligations. Although our management believes that the incurrence of long-term indebtedness has been important in the development of our business, including facilitating our acquisitions of Insignia and Trammell Crow Company, the cash flow necessary to service this debt is not available for other general corporate purposes, which may limit our flexibility in planning for, or reacting to, changes in our business and in the commercial real estate services industry. Notwithstanding the actions described above, however, our level of indebtedness and the operating and financial restrictions in our debt agreements both place constraints on the operation of our business.

As Americans realize that they don’t “need” a $5 Starbucks latte, IKEA knickknacks, Jimmy Choo shoes, Rolex watches, granite counters, and stainless steel appliances, our mall centric world will end. Major mall anchor retailers Macy's (M), JC Penney (JCP), and Sears (SHLD) are in for a heap of trouble in the next few years. As low prices become the only factor that drives retail sales, retailers will have minimal profits in the future, further restricting expansion and renovations.

Mall developer General Growth Properties, which owns or operates 200 malls, added $4 billion of debt in the last three years and is teetering on the brink of bankruptcy. Simon Properties, which owns or operates 320 malls, added $3 billion of debt in the last three years and will be greatly affected by the coming downturn. Many smaller developers will be in even more dire straits. With shrinking cash flow, looming debt refinancing, and dim prospects for a resumption of conspicuous consumption, Mall developers are destined for a bleak future. Picture Clint Eastwood from his spaghetti western days riding a horse through the middle of your local mall with tumbleweeds blowing past the vacant KB Toys and Victoria's Secret.

(Note: You can view every article as one long page if you sign up as an Advocate Member, or higher).